Advanced SO? Removal: Guantong’s CFB Semi-Dry & Dry Sorbent Injection (DSI) Systems for Global Emission Control

1. Introduction: The Global Crossroads of Emission Control Policy

The global industrial landscape faces a critical juncture. As environmental awareness intensifies, regulations governing airborne pollutants like sulfur dioxide (SO?) and nitrogen oxides (NOx) are becoming increasingly stringent, yet the approaches vary significantly across major economic zones. In the European Union, a penalty-driven system enforces strict emission limits, demanding rapid technological adoption. Conversely, the United States employs a mix of established EPA regulations and newer, incentive-led programs, particularly around clean energy initiatives.

This policy divergence creates complex challenges for multinational corporations and industrial operators. Navigating these differing requirements demands sophisticated Flue gas desulfurization (FGD) and Denitrification strategies. Illustrative examples highlight the stakes: EU non-compliance can trigger annual penalties potentially exceeding €3 million for a large facility, while aligning with US clean energy goals, such as those in the Inflation Reduction Act (IRA), could unlock potential tax credits worth millions over a decade, if strict emission prerequisites are met.

The key lies in deploying adaptable, high-performance emission control technologies. Jiangsu Guantong Shengshi Intelligent Technology Co., Ltd. (Guangtong) specializes in precisely this area. Our integrated approach, often combining advanced Circulating Fluidized Bed (CFB) semi-dry FGD with optimized Selective Catalytic Reduction (SCR) Denitrification systems, offers a tailored pathway to meet diverse global standards, potentially cutting compliance and operational costs by up to 30% compared to traditional methods. This post explores the policy divide, market trends, technological solutions, and economic considerations essential for mastering global emission control.

2. Policy Analysis: Regulatory Mandates vs. Fiscal Incentives

Understanding the distinct regulatory philosophies of the EU and US is crucial for strategic planning.

2.1 EU’s Zero-Emission Drive: The Industrial Emissions Directive (IED)

The EU leads with a mandate-heavy approach, primarily through the Industrial Emissions Directive (IED). Recent updates, effective from 2024, significantly tighten the screws:

- Stricter Limits: SO? emission limits for many large combustion plants are reduced to ≤15mg/Nm3 under the latest Best Available Techniques (BAT) reference documents (BREFs), representing a reduction of up to 60% from previous levels. NOx limits are similarly stringent.

- Rigorous Enforcement: Compliance is ensured through mandatory BAT certification, continuous real-time emissions monitoring (CEMS), and substantial financial penalties for exceedances, often linked to company revenue. Carbon pricing mechanisms (€100+/ton in some ETS phases) add further pressure.

- Real-World Consequences: Non-compliance is costly. For instance, reports indicate a Polish steel plant faced fines accumulating to €4.8 million in 2023 for failing to meet emission standards, demonstrating the EU’s enforcement resolve.

This regulatory environment necessitates investment in best-in-class Desulfurization and Denitrification technologies capable of meeting ultra-low emission values consistently.

2.2 US Approach: EPA Rules Meet Clean Energy Incentives

The US regulatory landscape is more multifaceted:

- Established EPA Oversight: Long-standing programs like the Cross-State Air Pollution Rule (CSAPR) and Mercury and Air Toxics Standards (MATS) continue to drive significant investment in FGD and SCR systems, particularly in the power sector, to meet regional and national air quality goals.

- IRA Incentives (45V Credits): The Inflation Reduction Act introduced powerful incentives, such as the 45V tax credit for clean hydrogen production. Critically, eligibility for the highest credit tier ($3/kg hydrogen) requires demonstrating very low lifecycle emissions, including stringent NOx limits (often cited around ≤0.035 kg NOx per MMBtu, aligning conceptually with targets like ≤35mg/Nm3) for grid electricity used in electrolysis. This creates a strong incentive for hydrogen producers using grid power to ensure their electricity source employs effective SCR Denitrification systems. Utilizing registered apprentices can multiply these credits fivefold.

- Compliance Flexibility: While stringent, some aspects, like the hourly power matching requirements for the 45V credit, have implementation timelines extending towards 2030, allowing phased adoption.

- Case Example: Guantong’s advanced SCR Denitrification system technology helped a Texas-based clean hydrogen project meet the rigorous NOx emission prerequisites tied to grid power sourcing, significantly enhancing its eligibility profile for substantial tax credits under the IRA 45V program.

Navigating the US market requires solutions that satisfy both baseline EPA regulations and the specific criteria of incentive programs like the IRA.

3. FGD Market Projections & Growth Drivers

The global Flue gas desulfurization system market is experiencing robust growth, driven by these diverse regulatory pressures and industrial expansion.

3.1 Global Market Outlook

According to recent analyses by Global Market Insights (GMI):

- 2024 Valuation: The market reached approximately $20.77 Billion.

- 2030 Forecast: It is projected to exceed $28 Billion, expanding at a Compound Annual Growth Rate (CAGR) of around 4.3%.

Key regional drivers include:

- EU (Approx. 28% Market Share): Driven by IED compliance, over 300 coal-fired power plant units require retrofits or upgrades with advanced FGD and DeNOx technologies.

- US (Approx. 18% Market Share): Fueled by both EPA regulations and new opportunities linked to around 120 new clean hydrogen projects and other industrial initiatives seeking low-emission operations.

- Asia-Pacific (Dominant 48% Share): Led by China and India, continued reliance on coal for power generation and industrial growth necessitates massive investments in emission control, including FGD.

3.2 Regional Deep Dive

- China: Continues large-scale deployment, with over 500 major wet FGD installations achieving high SO? removal rates (often >95%). Guantong, as a leading domestic supplier, leverages its extensive experience here.

- India: Faces significant challenges with ~12GW of new coal capacity planned, requiring an estimated $1.2 Billion in FGD investments in the near term to meet national standards. Cost-effective and reliable solutions are paramount.

- EU: A notable shift towards dry and semi-dry technologies, particularly CFB systems, is underway due to stricter limits and water scarcity concerns. CFB adoption is projected to capture up to 35% of the EU FGD market share by 2025.

Guantong’s diverse portfolio, featuring high-efficiency CFB systems ideal for the EU, proven wet FGD capabilities relevant to Asia, and advanced SCR technology suited for US requirements, positions us to serve these varied global demands effectively.

4. Technology Trends: Wet, Dry, Semi-Dry & SCR Systems

Selecting the right emission control technology depends on specific regulations, fuel types, plant size, and economic factors.

4.1 Wet FGD Dominance & Evolution

What is flue gas desulfurization (FGD)? It’s a vital industrial process designed to remove sulfur dioxide (SO?) – a primary component of acid rain and a respiratory irritant – from the exhaust gases (flue gases) of power plants and industrial facilities burning fossil fuels or processing sulfur-containing materials. Why is flue gas desulfurization important? It’s essential for protecting public health and the environment, enabling industries to operate within strict air quality regulations.

How does wet flue gas desulfurization work? The most established type, Wet FGD, currently holds about 60% of the global market share. Typically, it involves contacting flue gas with an alkaline slurry, most commonly limestone (CaCO?) or lime (CaO). The SO? reacts with the slurry to form calcium sulfite (CaSO?) or, after forced oxidation, calcium sulfate (CaSO?), also known as synthetic gypsum.

- Pros: High SO? removal efficiency (>95% achievable), produces saleable gypsum byproduct.

- Cons: High water consumption (e.g., potentially 800 m3/day for a large plant), significant energy requirements for pumps and fans, and potentially large equipment footprint leading to higher operational expenditure (OPEX) – sometimes estimated around $1.4M/year for large units.

4.2 The Rise of Dry & Semi-Dry FGD: Efficiency Meets Sustainability

Driven by water scarcity and the need for ultra-low emissions, dry and semi-dry FGD methods are gaining prominence, especially Circulating Fluidized Bed (CFB) semi-dry desulfurization:

- CFB Systems: These systems inject a hydrated lime sorbent into a reactor where it mixes turbulently with the flue gas. Water is often sprayed in to cool the gas and enhance the reaction. Key advantages include:

- Lower Water Use: Up to 60-70% less water consumption compared to wet FGD.

- High Efficiency: Capable of achieving SO? ≤10mg/Nm3, meeting the strictest EU IED limits.

- Guantong’s Expertise: We leverage advanced CFD flow field simulation to optimize reactor design, ensuring intense mixing, efficient sorbent utilization through internal and external recirculation, and stable performance. Our successful implementation at the Cabot XuYang Chemical (Xingtai) Co., Ltd. facility demonstrates achieving SO? ≤10mg/Nm3 and Dust ≤5mg/Nm3.

- Other Dry Systems (e.g., NID, Spray Dry Absorption – SDA): Technologies like Novel Integrated Desulphurization (NID) or SDA offer simpler designs, suitable for smaller plants or specific applications, often achieving SO? removal rates around 85-95%. Guantong also offers Dry Sorption (DS) technology using sodium bicarbonate for rapid reactions.

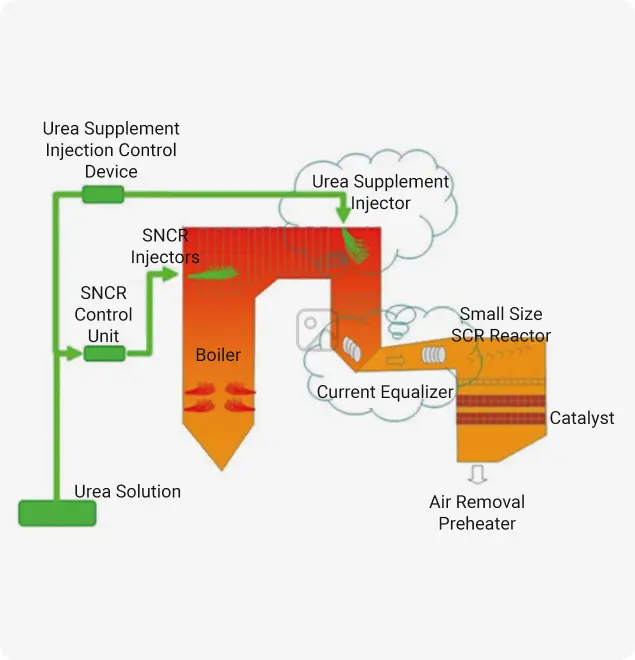

4.3 SCR Denitrification: Tackling NOx Emissions

Selective Catalytic Reduction (SCR) is the leading technology for high-efficiency NOx removal.

- How it Works: Ammonia (NH?), either directly injected or generated from urea, is introduced into the flue gas upstream of a catalyst bed. Within the catalyst (typically operating at 270-400°C), the NH? selectively reacts with NOx (NO and NO?) to form harmless nitrogen (N?) and water (H?O).

- Regulatory Alignment: Essential for meeting stringent NOx limits under EU IED/BREFs and US EPA regulations (like CSAPR). Also critical for enabling projects to qualify for US IRA incentives requiring low NOx footprints.

- Guantong’s Optimization:

- CFD & CKM: We utilize detailed CFD modeling and Chemical Kinetic Modeling (CKM) to determine optimal ammonia injection grid (AIG) design, placement, and control strategies, maximizing NOx reduction while minimizing ammonia slip (unreacted NH?) and ensuring catalyst longevity (often targeting 3.5+ years).

- Urea-to-Ammonia: Recognizing safety concerns with liquid ammonia transport and storage, Guantong provides reliable Urea Pyrolysis Furnace Equipment. This turnkey system safely generates ammonia on-site from readily available urea, a significant advantage in regulated or safety-conscious areas. Our successful Cabot Tianjin SCR project showcases this capability.

An effective SCR denitrification system is indispensable for comprehensive emission control strategies globally.

[Image: Schematic of an SCR Denitrification System showing ammonia injection and catalyst layers]

5. Economic Analysis: Cost-Benefit Breakdown of FGD Choices

Choosing between Wet FGD and advanced Semi-Dry options like CFB involves a careful economic assessment. The following table provides an illustrative comparison for a typical large industrial application:

| Parameter | Conventional Wet FGD | Guantong CFB Semi-Dry | Savings / Advantage |

| CAPEX (Illustrative) | ~$25 Million | ~$18 Million | ↓28% (Lower equipment/footprint) |

| OPEX/Year (Illustrative) | ~$1.4 Million | ~$1.02 Million | ↓27% (~$380K/year, lower energy/sorbent) |

| Water Use | ~800 m3/day | ~300 m3/day | ↓62.5% (Significant in water-stressed areas) |

| Compliance Achieved | SO? ~50mg/Nm3 (Typical) | SO? ≤10mg/Nm3 (Meets EU IED) | Higher Compliance Assurance |

| Byproduct Revenue | ~$0.1M (Gypsum Sale) | ~$0.05M – $0.1M (Mixed salts disposal/potential use) | Varies; focus on OPEX/CAPEX savings |

Interpretation: While Wet FGD can generate higher-quality gypsum, the significant reductions in Capital Expenditure (CAPEX), Operational Expenditure (OPEX), and particularly water usage often make CFB Semi-Dry systems more economically attractive, especially when facing stringent emission limits like those in the EU. The lower OPEX translates directly to improved profitability and faster ROI, further amplified by avoiding potential non-compliance penalties. This data helps clarify the FGD meaning in practical financial terms.

6. Corporate Strategies for Dual Compliance & Optimization

Successfully navigating the global emissions landscape requires tailored strategies:

6.1 EU Action Plan: Prioritize Compliance & Efficiency

- Retrofit Focus: For plants >300MW or those facing imminent IED limits, prioritize retrofitting with high-efficiency systems like Guantong’s CFB Semi-Dry FGD. Leverage its proven ability to meet SO? ≤10mg/Nm3 for a rapid ROI (often achievable within 3-5 years considering penalty avoidance).

- BAT Certification Support: Utilize Guantong’s comprehensive performance data, operational guarantees, and ISO 9001 quality management system documentation to support your BAT compliance submissions to regulatory authorities.

6.2 US Optimization: Leverage Regulations & Incentives

- Integrated SCR Design: Embed advanced SCR Denitrification systems early in Front-End Engineering Design (FEED) studies for new projects or major upgrades, ensuring compliance with EPA standards and maximizing potential eligibility for IRA credits where applicable. Leverage Guantong’s CFD and Urea Pyrolysis expertise for optimized, safer designs.

- Incentive-Focused Labor Strategy: For projects targeting IRA 45V credits, ensure workforce planning includes the required percentage of registered apprentices (often 10-15% depending on project start date) to secure the 5x credit multiplier.

6.3 Cross-Border Synergy: Consistency & Control

- Standardized Technology: Employ consistent, high-performance technology like Guantong’s CFB and SCR systems across global operations where feasible, simplifying maintenance, spare parts management, and operator training.

- Turnkey Solutions: Leverage Guantong’s capability to deliver turnkey (EPC – Engineering, Procurement, Construction) projects, ensuring quality control from design through commissioning, regardless of location.

- Unified Monitoring Potential: Explore integrated monitoring solutions (potentially leveraging Guantong’s control system interfaces or third-party platforms) to track SO?/NOx performance across your global asset portfolio in near real-time.

7. Regional Success Stories: Guantong Technology in Action

- EU Example (Italy): Power Plant Achieves €2.2M+ Annual Savings

- Challenge: An Italian power plant needed to meet tightened IED SO? limits and reduce operational costs.

- Solution: Retrofitting with Guantong’s CFB Semi-Dry FGD system.

- Outcome: Achieved consistent SO? emissions below 10mg/Nm3, resulting in estimated annual savings exceeding €2.2 Million through avoided penalties and over 35% reduction in water consumption costs.?

- Asia-Pacific Opportunity (India): Supporting National Growth

- Market Need: India’s planned 12GW coal power expansion requires reliable, cost-effective FGD solutions. Market estimates suggest over $480 Million in FGD contracts will be awarded between 2024-2026.

- Guantong’s Role: We are actively engaging with partners and clients in India, offering proven FGD and Denitrification technologies tailored to meet local requirements and budgets.

- US Example (Louisiana): Chemical Plant Enhances Competitiveness

- Challenge: A Louisiana chemical facility sought to significantly reduce NOx emissions to meet stringent permit levels and improve its environmental profile.

- Solution: Installation of a Guantong SCR Denitrification system, optimized using CFD modeling.

- Outcome: Successfully reduced NOx emissions to below 32mg/Nm3, ensuring regulatory compliance and enhancing the plant’s operational license and community standing. This performance level aligns with the requirements sought by projects aiming for federal clean energy incentives, potentially improving the plant’s future project economics (illustrative IRR impact often cited at 20%+ for such upgrades).?

8. Conclusion: Winning the Global Emission Control Game

The diverging paths of global environmental policy present both challenges and opportunities. Mastering this landscape requires strategic investment in adaptable, high-performance emission control technologies.

By adopting advanced solutions like Guantong’s integrated CFB-SCR approach, industrial operators can:

- ? Secure Compliance: Confidently meet stringent EU IED limits (e.g., SO? ≤10mg/Nm3).

- ? Capture Opportunities: Satisfy US EPA regulations and unlock potential clean energy incentives (e.g., NOx ≤35mg/Nm3).

- ? Drive Efficiency: Reduce operational costs through lower water and energy consumption.

- ? Enable Growth: Profitably participate in high-growth markets like the Asia-Pacific region (forecasted at 6.35% CAGR in some segments).

Don’t let complex regulations hinder your global operations. Partner with Guantong for tailored, future-proof Flue gas desulfurization and Denitrification solutions.

Take the Next Step:

- ?? Request a Plant Audit & Consultation: Contact Mr. Yang at 0086-13773732788 or visit our contact page to discuss your specific needs.?